RAYMOND JAMES FINANCIAL STOCK ANALYSIS

- Dec 2, 2025

- 8 min read

Products and Services

Raymond James Financial provides financial planning, investment advisory services, brokerage trading, and distribution of mutual funds, annuities, and insurance. It also offers investment banking services such as M&A advice and securities underwriting, along with institutional sales and trading. The firm manages assets through its asset management division and operates a bank that provides securities-based loans, mortgages, commercial lending, and insured deposit accounts.

Pricing Strategy

The firm charges asset-based fees for advisory accounts and managed portfolios. It earns commissions on securities trades and on sales of funds, annuities, and insurance products. Investment banking fees depend on the size and completion of transactions. The banking division earns net interest income by lending at higher rates than it pays on deposits. Additional revenues come from account fees, custodial fees, and servicing fees from partner banks.

Sales Channels

Raymond James reaches most clients through a large network of financial advisors who operate in employee and independent models. Services are also delivered through branch offices, advisor run practices, digital platforms, and mobile tools. Institutional clients interact through investment bankers, traders, and research teams. The bank division serves clients through online access, loan officers, and referrals from advisors.

Customers Base

The firm serves retail investors, including mass affluent and high net worth households who use its financial advisors for planning and investing. It also serves corporations, municipalities, nonprofits, and institutional investors that rely on its investment banking and trading services. In addition, independent RIAs and broker dealers use Raymond James for custody, execution, research, and operational support. Banks and insurers also interact with the firm through deposit programs and tax credit investments.

Supply Chain

Raymond James depends on financial advisors, bankers, traders, portfolio managers, and technology and compliance teams. It relies on trading systems, planning tools, clearing organizations, exchanges, and third-party product providers. The bank requires strong capital resources, liquidity, and regulatory infrastructure. The firm also works with developers and institutional buyers in its tax credit housing business and with partner banks in its deposit programs.

REVENUE DRIVERS

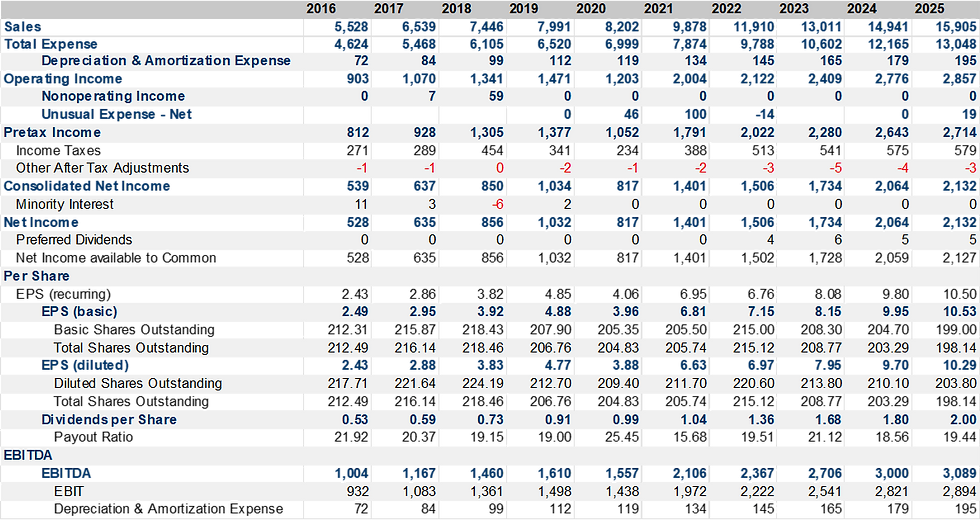

Raymond James’ revenues are heavily concentrated in the Private Client Group segment, which accounts for nearly 70 percent of total sales. This share has remained fairly steady over time, indicating that the company has not made any major changes in how it operates or delivers its services, which is typical for firms in the financial services industry. The other segments have also shown similar stability, with the exception of the banking segment, which has gradually increased its contribution to total revenue. The analysis also shows that RJF’s overall revenue has followed an upward trend for the past ten years, although the growth rate has been inconsistent. Growth has ranged from as low as 3.22 percent in 2020 to as high as 21.67 percent in 2021, a jump that was most likely the result of recovery following the Covid 19 pandemic period.

INDUSTRY & COMPETITION ANALYSIS

PORTER’S 5 FORCES

Competitive Rivalry

High

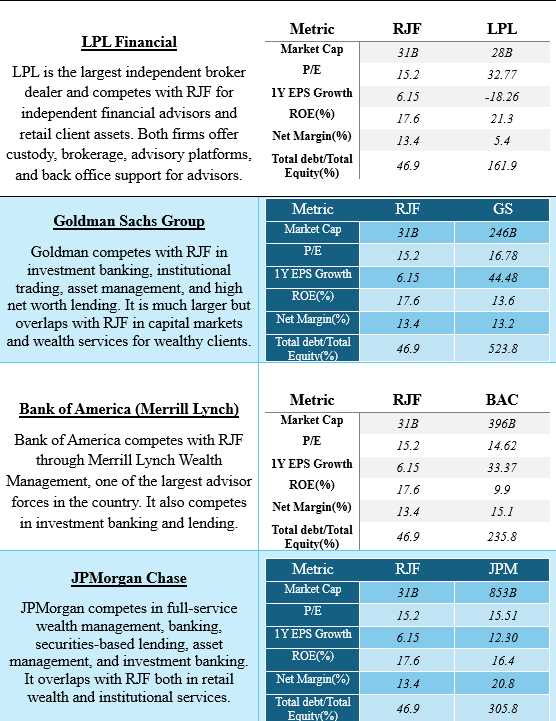

RJF faces strong competition from full service wealth managers like Morgan Stanley, Merrill Lynch, UBS, and Wells Fargo Advisors, as well as independent broker dealers such as LPL and Ameriprise. It also competes with major investment banks such as Goldman Sachs and JPMorgan in capital markets. The industry has many well capitalized firms, similar product offerings, intense advisor recruiting battles, and high client switching based on trust and performance. This makes rivalry high.

Threat of New Entrants

Moderate to Low

Entering the wealth management, brokerage, and banking industries requires high regulatory approval, significant capital, and advanced technology infrastructure. These barriers make it difficult for new full scale firms to enter. However, fintech platforms like Webull and Robinhood can enter the self directed trading segment more easily. This makes the overall threat low for full service competitors but moderate in retail trading.

Bargaining Power of Buyers (Clients)

Moderate to High

Clients have many choices for financial advisors, custodians, trading platforms, and banks. Switching costs can be low for transactional clients and moderate for advisory relationships. High net worth clients demand competitive pricing, strong service, and advisor expertise. Institutional clients also negotiate fees aggressively in investment banking and asset management. This creates moderate to high buyer power.

Bargaining Power of Suppliers

Moderate

RJF depends on financial advisors, technology vendors, exchanges, clearing firms, and third party product providers such as mutual fund and insurance companies. Financial advisors in particular have high power because they can switch firms, and firms often pay large recruiting packages. Technology providers and market data vendors also have influence. This makes supplier power moderate.

Market Share in Retail Advisory and Brokerage Services

According to FactSet data, RJF currently holds approximately 17.13 percent of the revenue in the retail advisory and brokerage services industry. With the industry generating an estimated 62.3 billion dollars, the firm controls a sizable portion of a highly competitive market where substitutes are readily available to customers.

DUPONT ANALYSIS

VALUATION

Earning Power Value Per Share

We value this firm by using the earning power value method which aims to provide a clear picture of the earnings capacities of the firm’s stock based on current operations, without taking future growth into account. This method attempts to estimate what each stock of the firm is worth now, as current conditions stands.

To achieve this calculation, we use the firm’s most recent sales value as their sustainable earnings value. We assume their operating margin and income tax rate to be respectively 18% and 22%, reflecting the firm’s performance in the past few years. The resulting NOPAT is divided by our calculated WACC to obtain RJF’s total earning power value.

We added the total cash and total debt to that value to derive the total equity value of the firm, which, divided by the total shares outstanding, renders an estimate of the intrinsic value of the share as representation of its earning power.

Earnings Multiple Valuation

For this valuation method, we estimate the value of Raymond James stock by using industry multiples. Our comparison includes three groups: the competitors described earlier, the firms classified under the S&P 500 Capital Markets industry, and the entire Financials sector of the S&P 500. The multiples used are the current and one year forward P/E ratios and the P/BV ratio.

This approach shows that Raymond James appears to be underpriced relative to the average earnings and book value multiples of the top firms in its industry, which suggests that the stock is an attractive buying opportunity.

INVESTMENT RISK

Market Risk: RJF is currently priced at 15 times its earnings, which implies that the stock is fairly priced in the market context. With also a beta of 1.12, RJF’s valuation moves closely with the overall market. Because of that, market risk seems to be very low and a significant drop in Raymond James’ value would likely be accompanied by a concurrent market crash.

Financial Risk: RJF financial picture looks very strong, with a low debt to capitalization ratio, a strong cash position and A- credit rating from S&P. The firm has been constantly growing its revenue while having very low debt positions.

Credit and Lending Risk: RJF’s bank segments hold securities-based loans, corporate loans, mortgages, and tax-exempt loans. These expose the firm to borrower defaults, collateral value declines, and changes in credit conditions. Although SBLs are secured by marketable securities, falling markets or insufficient collateral can increase credit losses.

Interest Rate Risk: A significant portion of RJF’s earnings comes from net interest income in its bank operations and from deposit programs. Changes in interest rates affect loan yields, deposit costs, and investment portfolio income. Rising rates can increase funding costs, while falling rates can squeeze margins and reduce RJBDP sweep-fee revenue.

APPENDIX

Income Statement

WACC

MANAGEMENT

Paul M. Shoukry, MBA, CPA

President, Chief Executive Officer

Paul M. Shoukry has served as President, Chief Executive Officer, and Director of Raymond James Financial since 2025. He is also a Director of TriState Capital Bank and ReliaQuest LLC, and he sits on the Board of Trustees at Academy Prep Center of Tampa. His career at Raymond James began in 2010, and he previously held senior roles including Chairman of the Tampa Bay Heart Ball at the American Heart Association. Mr. Shoukry earned his MBA from Columbia University in New York and completed his undergraduate studies at the University of Georgia. He is involved in various community and charitable organizations and has built a strong reputation for leadership within the firm.

________________________________________________________________________

Scott Alan Curtis, MBA

Chief Operating Officer

Scott Alan Curtis serves as Chief Operating Officer of Raymond James Financial and holds additional leadership roles across the company. He has been with Raymond James since 2018 and currently chairs the Financial Industry Regulatory Authority Institute. He also serves as Director of Raymond James Ltd. His prior experience includes senior roles at GE Financial Assurance Holdings, Raymond James Insurance Group, and positions at Waddell and Reed Financial Advisors. Mr. Curtis holds an MBA from the Stephen M. Ross School of Business and completed his undergraduate degree at Denison University. His responsibilities span operational management, strategic oversight, and advisor support across the Raymond James platform.

________________________________________________________________________

Jonathan W. Oorlog, Jr., CPA

Chief Financial Officer

Jonathan W. Oorlog is the Chief Financial Officer of Raymond James Financial. He has served in this role since 2024 and has been with the firm since 2014. He is also the Chief Financial Officer of Raymond James Affordable Housing Investments, a position he has held since 2004. His previous roles include Chief Financial Officer and Vice President at Gateway Tax Credit Fund II Ltd. and Gateway Tax Credit Fund III Ltd., as well as Chief Financial Officer at Cellector Corp. Mr. Oorlog earned both his undergraduate and graduate degrees from Florida State University and has more than two decades of experience in financial leadership and tax credit investment operations.

________________________________________________________________________

Andy Zolper

Chief Information Officer

Andy Zolper serves as the Chief Information Officer at Raymond James Financial, a position he has held since 2012. He joined the company the same year and has been responsible for overseeing the firm’s information technology strategy, cybersecurity initiatives, and the development of systems that support advisors, clients, and internal operations. Under his leadership, the firm has strengthened its technological infrastructure and enhanced digital capabilities across its wealth management and capital markets businesses.

________________________________________________________________________

Vin Campagnoli

Executive Vice President of Technology and Operations

Vin Campagnoli serves as the Executive Vice President of Technology and Operations at Raymond James Financial. He has been with the company since 2011 and oversees the firm’s technology strategy, operations infrastructure, and digital innovation initiatives. His work supports financial advisors, clients, and internal teams across all business segments. Under his leadership, Raymond James has continued to modernize its platforms, strengthen cybersecurity, and enhance operational efficiency.

________________________________________________________________________

Rich Konefal

Chief Compliance Officer

Rich Konefal is the Chief Compliance Officer at Raymond James Financial. In this role, he is responsible for overseeing the firm’s compliance programs, regulatory adherence, supervisory systems, and risk controls across the organization. His work ensures that the company meets all industry regulations and maintains strong oversight within its wealth management, capital markets, banking, and asset management businesses.

________________________________________________________________________

Jonathan N. Santelli

Secretary, Executive Vice President and General Counsel

Jonathan N. Santelli joined the company in 2016 and oversees the firm’s legal, regulatory, and corporate governance functions. Prior to his current role, he was the General Counsel for Private Wealth Management at Bank of America from 2009 to 2013. From 2013 to 2016, he held the position of Senior Vice President and Deputy General Counsel at First Republic Bank in San Francisco.

ESG ANALYSIS

Reach out to the author of this analysis at mberotte@aglaosconsulting.com

Download the full report below.

The information contained in this report is for educational and informational purposes only and does not constitute investment advice or a recommendation to buy, sell, or hold any security. Data sources include company filings, FactSet, Yahoo Finance, and other publicly available information. Analysis may incorporate proprietary models, Python programming, Microsoft Office applications, and AI-assisted drafting tools. While efforts are made to ensure accuracy, Aglaos Consulting LLC does not guarantee the completeness or reliability of the information provided. Past performance is not indicative of future results.