Charles Schwab Stock Analysis

- Dec 9, 2025

- 8 min read

BUSINESS MODEL

Products and Services

Charles Schwab offers a broad suite of financial services, including brokerage accounts for trading stocks, bonds, ETFs, options, and futures, along with margin lending and cash-management tools. Schwab also provides proprietary and third-party mutual funds and ETFs, professionally managed investment portfolios, alternative investment access, banking products such as deposits, mortgages, HELOCs, and pledged-asset lines, as well as trust and custodial services. Together, these services give Schwab a fully integrated platform supporting investors’ trading, planning, advisory, and banking needs.

Pricing Strategy

Schwab uses a combination of interest-based, asset-based, and activity-based revenue models. The largest portion of revenue comes from net interest income on client cash and margin loans. Asset management and advisory fees are charged as a percentage of AUM for managed portfolios and proprietary funds. Trading revenue is generated from options commissions, order-flow payments, and fixed-income spreads, even though most stock and ETF trades are commission-free. Bank products earn interest spreads, while other administrative and service fees contribute additional revenue. Payment is typically ongoing (monthly or quarterly) based on account activity or asset levels.

Sales Channels

Schwab acquires and serves clients through a multichannel system combining digital platforms, service centers, and physical branches. Most clients engage digitally through Schwab.com and the Schwab Mobile app for trading, banking, research, and education. Phone-based support and 24/7 service centers help with more complex needs, while branches and financial consultants build deeper, relationship-driven advisory connections. RIAs are supported through dedicated sales teams, technology platforms, and national or regional events. All products are delivered via Schwab's integrated digital ecosystem and human specialist network.

Customers Base

Schwab serves three main groups: everyday retail investors, independent financial advisors (RIAs), and corporate clients. Retail clients range from beginner investors to high-net-worth households seeking advisory and wealth management support. RIAs use Schwab as a custodian, leveraging its trading, technology, and banking infrastructure to serve their own clients. Corporate clients include retirement plan sponsors, stock plan administrators, and institutions using Schwab’s clearing, custody, and recordkeeping solutions.

Supply Chain

To operate efficiently, Schwab relies on scalable technology infrastructure, including trading systems, advisory platforms, and digital tools inherited from both Schwab and Ameritrade. It partners with TD Bank for client cash sweep programs and works closely with exchanges, clearing firms, fund managers, and third-party software providers. Internally, Schwab depends on its financial consultants, advisor-support teams, and call-center infrastructure to deliver service/

REVENUE DRIVERS

Schwab’s net interest revenue currently represents nearly half of its total annual sales, underscoring a major weight in the company’s revenue composition. A closer examination reveals that interest income alone accounts for an extraordinary 79% of total revenue, up from 46% a decade ago. This 33-percentage-point increase highlights a growing dependence on interest-driven activities. At the same time, the company’s interest expense has surged dramatically, jumping from –7% to –35% in 2023, a fivefold increase. Together, these trends illustrate a firm increasingly oriented toward lending and cash-driven revenue streams, while also relying more heavily on debt and higher-cost funding to support its operations.

Conversely, Schwab’s asset management business has contracted over the same period, declining from 40% to 30% of total revenue. Trading revenue has been inconsistent as well, falling from 11% to 7%, then rebounding sharply to 22% in 2021 before tapering off again by 2025. Overall, the company’s revenue mix has shifted away from fee-based and trading activities and toward a more interest-sensitive model, exposing Schwab to greater volatility tied to interest rate cycles and funding costs.

INDUSTRY & COMPETITION ANALYSIS

PORTER’S 5 FORCES

Competitive Rivalry

High

Competitive rivalry in the brokerage and wealth management industry is very high. Schwab competes with large, well-established firms such as Fidelity, Vanguard, Morgan Stanley, JPMorgan, Goldman Sachs, and Interactive Brokers. Many competitors offer commission-free trading, low-cost ETFs, and advanced digital platforms, which puts pressure on pricing and innovation. Product differentiation is limited in retail brokerage, which intensifies competition. Rivalry is further strengthened by aggressive marketing, technological advancement, and rising client expectations for digital convenience.

Threat of New Entrants

Moderate to Low

The threat of new entrants is moderate. It is relatively easy for fintech companies to launch basic investing apps, but difficult to build the scale, trust, capital, and regulatory expertise required to compete with Schwab. Barriers include strict SEC and FINRA regulations, high compliance costs, advanced technology infrastructure requirements, and the need for brand credibility in handling client assets. New entrants like Robinhood have shown that disruption is possible, but replicating Schwab’s scale in custody, banking, and advisory services remains challenging.

.

Bargaining Power of Buyers (Clients)

Moderate to High

Customer bargaining power is high. Investors have many competing brokerage options that offer similar features at low or zero cost. Switching costs are low since transferring brokerage accounts is simple and often free. Clients also have access to abundant information, investment tools, and mobile platforms, which strengthens their negotiating position. Price sensitivity has grown significantly since the industry moved to zero commissions, pushing firms to compete on interest rates, platform features, and advisory services.

Bargaining Power of Suppliers

Moderate

Supplier power is moderate. Schwab relies on technology providers, market makers, exchanges, and financial product issuers. Exchanges and clearing firms have some power due to the essential nature of their services. Fund managers and ETF providers have limited influence because Schwab offers its own index products and can substitute third-party funds. Custodial and banking operations require strong technology infrastructure, and dependence on external systems can create switching challenges. Overall supplier power exists but is not dominant.

Market Share in Retail Advisory and Brokerage Services

According to FactSet data, Schwab currently holds approximately 33% of the revenue in the retail advisory and brokerage services industry. With the industry generating an estimated 62.3 billion dollars, controlling a third of these revenues is a testimony of Schwab’s dominance in terms of market share

DUPONT ANALYSIS

VALUATION

Earning Power Value Per Share

We value this firm by using the earning power value method which aims to provide a clear picture of the earnings capacities of the firm’s stock based on current operations, without taking future growth into account. This method attempts to estimate what the stock is worth now, as current conditions stand.

Sensitivity Analysis

To achieve this calculation, we use the firm’s most recent sales value of 27.1B as their sustainable earnings value.

We reevaluated the firm’s expenses by using their capital expenditure on fixed assets as the true estimation of D&A, which increased the true operating margin from 45 to 48%. We also used an estimated tax rate of 23%, reflecting current corporation taxation. The resulting NOPAT is divided by our calculated WACC of 8.31% to set Schwab’s sustainable earning power value at 121 billion.

We added the total cash and total debt to that value to derive the total equity value of the firm, which, divided by the total shares outstanding, renders a $83.12 estimate of the intrinsic value for the share, as a representation of its current earning power.

Earnings Multiple Valuation

For this valuation method, we estimate the value of Charles Schwab stock by using industry multiples. Our comparison includes three groups: the competitors described earlier, the firms classified under the S&P 500 Capital Markets industry, and the entire Financials sector of the S&P 500. The multiples used are the current and one year forward P/E ratios and the P/BV ratio.

This approach shows that Charles Schwab appears to be overpriced relative to the average earnings and book value multiples of the top firms in the industry.

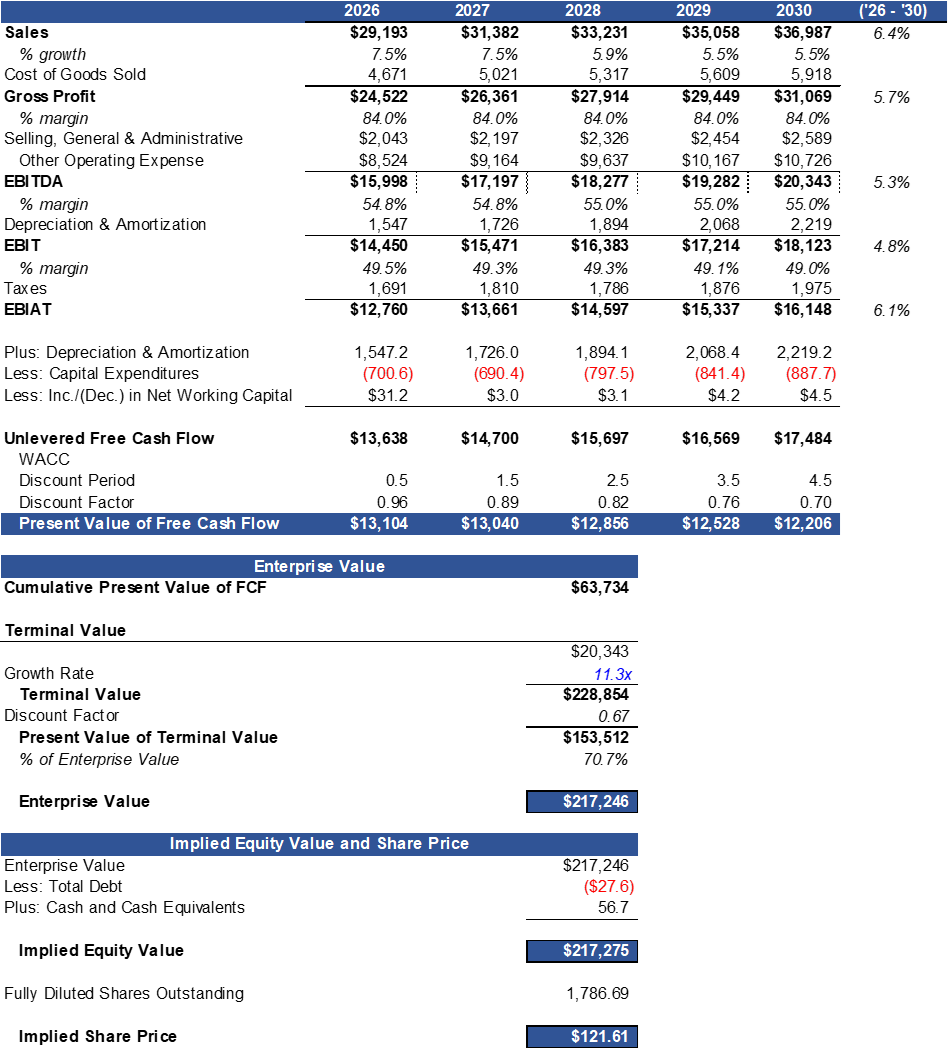

Discounted Cash Flow

INVESTMENT RISK

Market Risk: Schwab is currently priced at 22 times its earnings, which is more or less equal to the average price to earnings ratio of financial firm in this sector. It’s beta of 1.09 also implies that the stock moves in tandem with the market and any price volatility should correspond to the overall market behavior.

Business Risk: Schwab’s business is in current good standing. As is expected for such a high-profile firm, management is composed of highly skilled and experienced members which investors can trust to conduct the firm’s business operations. Over the past 10 years, they have averaged a gross margin and net margin of respectively 85% and 27%, which are slightly higher than the average margins of similar firms. They have also kept a stable return on invested capital (except in 2023) and consistently growing sales per share.

Financial Risk: Schwab financial picture looks very strong, with a strong cash position and A- credit rating from S&P. With exception to the year 2023, the firm has been constantly maintaining a low weight of its net debt on its total equity and its total capital.

Interest Rate Risk: 80% of Schwab’s earnings come from interest income. Changes in interest rates affect loan yields, deposit costs, and investment portfolio income. Rising rates can increase funding costs, while falling rates can squeeze margins and reduce the firm’s revenue.

APPENDIX

Organic Case (values in millions)

Bear Case (values in millions)

Bull Case (values in millions)

WACC

MANAGEMENT

Rick Wurster, CFA, MBA

President and Chief Executive Officer

Rick Wurster is the President and CEO of The Charles Schwab Corporation. He joined Schwab in 2021 after holding senior leadership roles across Schwab Investment Advisory, Schwab Investment Management, and Windhaven Investment Management. His earlier experience includes positions at Wellington Management, McKinsey, and Bain. He holds a degree from Villanova University and an MBA from the Tuck School of Business at Dartmouth.

__________________________________________________________________________________

Jason Clague, CFA, MBA

Managing Director and Head of Operations

Jason Clague is the Managing Director and Head of Operations at Charles Schwab, a role he has held since 2017. He has been with the firm since 2009 and focuses on operational leadership and firm-wide process improvement. He holds an MBA from Babson College and a bachelor’s degree from St. Lawrence University.

__________________________________________________________________________________

Michael Verdeschi, MBA

Chief Financial Officer and Managing Director

Michael Verdeschi is the Chief Financial Officer and a Managing Director at The Charles Schwab Corporation and Charles Schwab & Co. Inc. He joined Schwab in 2024 after serving as Treasurer at Citigroup. Mr. Verdeschi holds both his undergraduate degree and MBA from Iona College.

__________________________________________________________________________________

Dennis Howard

Chief Information Officer and Managing Director

Dennis Howard serves as Chief Information Officer and Managing Director at The Charles Schwab Corporation. He has been with Schwab since 2014, previously holding senior roles in technology services and serving as an independent director at SolarWinds from 2020 to 2025. Mr. Howard earned his graduate degree from Baylor University and his undergraduate degree from the University of Texas at San Antonio.

__________________________________________________________________________________

Tim Heier

Chief Technology Officer and Managing Director

Tim Heier serves as Chief Technology Officer and Managing Director at The Charles Schwab Corporation. He joined the company in 1999 and has held the CTO role since 2014. Mr. Heier holds a graduate degree from California State University–East Bay and an undergraduate degree from the University of California, Berkeley.

__________________________________________________________________________________

Adele Taylor, MBA

Managing Director and Head of Workplace Services

Adele Taylor is the Managing Director and Head of Workplace Services at The Charles Schwab Corporation, a role she assumed in 2024. She previously served as Senior Vice President of Corporate Strategy and Development at Franklin Resources from 2021 to 2024. Ms. Taylor earned her undergraduate degree from Yale University and an MBA from Columbia Business School.

__________________________________________________________________________________

ESG ANALYSIS

Reach out to the author of this analysis at mberotte@aglaosconsulting.com

Download the full report below.

The information contained in this report is for educational and informational purposes only and does not constitute investment advice or a recommendation to buy, sell, or hold any security. Data sources include company filings, FactSet, Yahoo Finance, and other publicly available information. Analysis may incorporate proprietary models, Python programming, Microsoft Office applications, and AI-assisted drafting tools. While efforts are made to ensure accuracy, Aglaos Consulting LLC does not guarantee the completeness or reliability of the information provided. Past performance is not indicative of future results.