QUALCOMM STOCK OVERVIEW

- Apr 19

- 6 min read

SNAPSHOT

Ticker | QCOM | Market Cap | $145B |

Sector | Electronic Components | P/E | 28.14 |

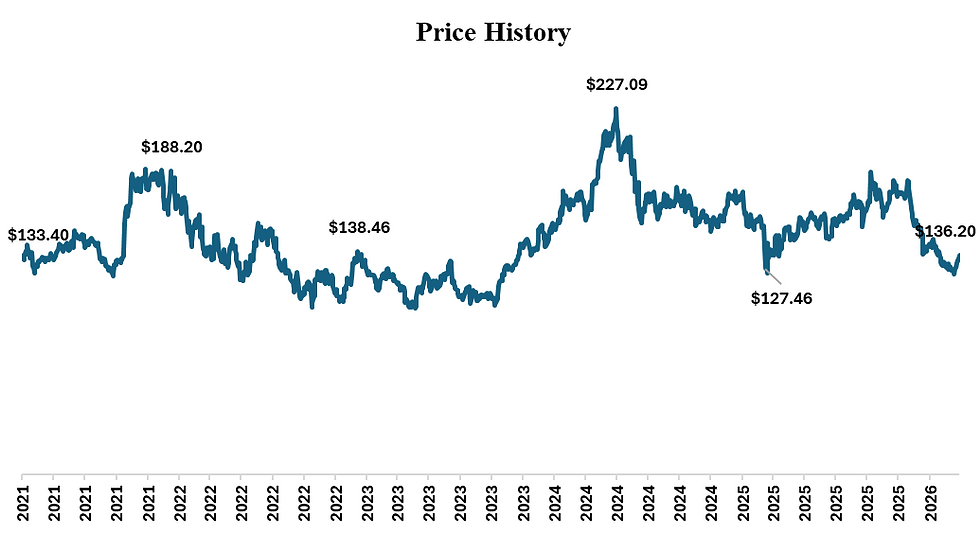

52 Week High-Low | $121.99 - $205.95 | 3 Year Beta | 1.40 |

CEO | Cristiano R. Amon | Target Price | $142.34 |

BUSINESS MODEL

Products Qualcomm operates a dual-engine model combining semiconductor design (QCT) and intellectual property licensing (QTL), monetizing both hardware and foundational wireless technologies. The company designs and sells highly integrated system-on-chip semiconductor platforms under Snapdragon and Dragonwing brands, which incorporate CPUs, GPUs, NPUs, connectivity modules, RF front-end systems, and AI processing capabilities for smartphones, automotive systems, and IoT devices. In parallel, Qualcomm licenses its extensive portfolio of standard-essential patents tied to 3G, 4G, and 5G wireless technologies, generating high-margin royalty revenue from global device manufacturers. This structure allows Qualcomm to capture value both at the component level and across the entire wireless ecosystem, with licensing acting as a structural profit anchor and semiconductors driving volume and ecosystem penetration. |

Customer Base Qualcomm’s customer base spans global OEMs, device manufacturers, automotive companies, IoT providers, and telecommunications ecosystem participants, including smartphone manufacturers, automotive OEMs integrating ADAS and digital cockpit systems, and enterprise and industrial IoT players. On the licensing side, hundreds of global companies producing wireless-enabled devices are required to license Qualcomm’s patent portfolio, effectively making Qualcomm a toll collector on the global cellular ecosystem. Demand is ultimately driven by end markets such as smartphones, connected vehicles, industrial automation, and edge computing devices, creating diversified exposure across consumer, enterprise, and industrial demand cycles. |

Pricing Method Qualcomm’s semiconductor pricing is determined by performance, integration level, and competitive positioning, with premium pricing power in high-end chipsets due to technological leadership in AI, connectivity, and power efficiency. In contrast, the licensing business generates revenue through per-unit royalties, typically calculated as a percentage of the wholesale selling price of licensed devices, often subject to caps and minimums. This hybrid pricing model creates a structurally attractive margin profile, where QTL delivers extremely high-margin, recurring revenue, while QCT pricing reflects cyclical semiconductor dynamics and competitive pressures. |

Supply Chain Qualcomm operates a fabless semiconductor model, outsourcing wafer fabrication, assembly, and testing to third-party foundries such as TSMC and Samsung, while maintaining internal design, architecture, and software capabilities. The company also produces certain RF front-end components internally, but the majority of production relies on global supply chain partners concentrated in Asia. This structure allows for capital efficiency but introduces dependency on external manufacturing capacity, geopolitical stability, and supply chain resilience. |

Sales Channels Semiconductor products are sold directly to OEMs and device manufacturers through supply agreements and purchase orders, while licensing revenue is generated through contractual agreements with device manufacturers worldwide. Qualcomm’s reach is amplified through its role in the broader wireless ecosystem, where its technologies are embedded across nearly all modern cellular-enabled devices. This creates a combination of direct hardware sales and indirect monetization through ecosystem-wide licensing. |

INDUSTRY ANALYSIS: PORTER'S 5 FORCES

Threat of New Entrants — Low The semiconductor and wireless IP industries have extremely high barriers to entry due to capital intensity, R&D requirements, patent portfolios, and ecosystem integration. Qualcomm’s decades-long investment in wireless standards and its extensive patent portfolio create a near-insurmountable moat, particularly in licensing, where participation in the cellular ecosystem effectively requires access to Qualcomm’s IP. New entrants can compete in specific chip segments, but replicating Qualcomm’s combined semiconductor and licensing ecosystem is structurally difficult. |

Bargaining Power of Buyers — Moderate to High Large OEM customers such as smartphone manufacturers and automotive companies exert significant negotiating power due to scale and potential vertical integration, including in-house chip design. The 10-K explicitly notes the risk of customers developing their own integrated circuits, which could reduce demand for Qualcomm’s products. However, Qualcomm retains leverage through technological leadership and essential IP, particularly in licensing, where buyers have limited alternatives. |

Bargaining Power of Suppliers — Moderate Qualcomm relies heavily on a concentrated set of advanced semiconductor foundries and assembly partners, which creates supplier dependency, particularly for leading-edge nodes. While Qualcomm’s scale provides some negotiating leverage, supplier power remains meaningful due to limited global fabrication capacity and the strategic importance of advanced manufacturing technologies. |

Threat of Substitutes — Moderate Substitution risk exists through alternative chip suppliers, internal chip development by OEMs, and shifts in technology architectures. However, Qualcomm’s integration of connectivity, AI, and power-efficient computing, along with its licensing model, reduces substitution risk at the ecosystem level, particularly in cellular standards where alternatives are limited. |

Competitive Rivalry — High The semiconductor industry is highly competitive, with rivals including vertically integrated firms and specialized chip designers. Competition is driven by performance, power efficiency, integration, price, and time-to-market. Rapid technological change, customer concentration, and potential industry consolidation intensify rivalry, especially as OEMs pursue vertical integration strategies. |

VALUATION: DISCOUNTED CASH FLOW

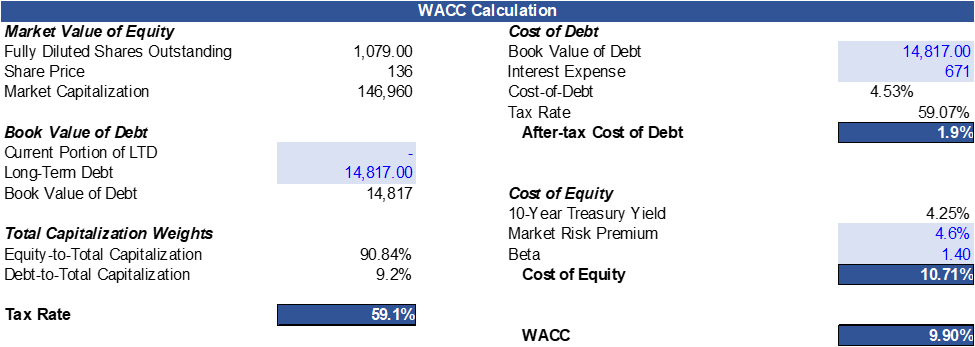

WACC

INVESTMENT RISKS

Systematic Risk |

Market Risk: Qualcomm trades at a P/E of 28.14 and EV/EBITDA of 11.05 with a WACC of 9.85%, reflecting a growth-oriented valuation tied to continued expansion in AI, automotive, and IoT. Revenue expectations remain strong with consensus EPS of 1.99 and a target price of $148.25, but valuation sensitivity is high given cyclicality in semiconductor demand. Profitability remains robust with gross margins around 55%, operating margins at 27.20%, and free cash flow margins at 28.81% in 2025, but the decline in net margin to 11.96% suggests earnings volatility and potential pressure from mix shifts or cost structures. |

Geopolitical Risk: Qualcomm faces elevated geopolitical risk due to its reliance on global supply chains and exposure to U.S.-China trade tensions, export controls, and regulatory environments. The company explicitly highlights risks related to international trade policies, national security restrictions, and supply chain disruptions, which can affect both semiconductor production and demand across key markets. |

Unsystematic Risk |

Business Risk: Business risk is driven by cyclicality in smartphone demand, customer concentration, and technological disruption. While diversification into automotive and IoT provides growth avenues, the core mobile segment remains critical. Metrics show declining return on invested capital from 26.96% in 2024 to 13.76% in 2025 and a drop in ROE to 21.48%, indicating reduced efficiency in capital deployment. Additionally, vertical integration by customers and rapid technological evolution pose ongoing risks to market share and pricing power. |

Financial Risk: Financial risk is relatively low to moderate, supported by strong coverage ratios and manageable leverage. Interest coverage remains high with EBIT/interest at 18.19x and EBITDA/interest at 20.51x, while total debt to EBITDA is approximately 1.08x, indicating conservative leverage. However, fluctuations in earnings and capital intensity in R&D could impact financial flexibility if margins compress. |

Liquidity Risk: Liquidity is solid, with a current ratio of 2.51 and quick ratio of 1.74 in 2025, supported by strong operating cash flow generation. CFO to current liabilities at 146.51% indicates strong short-term coverage, while free cash flow conversion has improved significantly to 169.88%, suggesting efficient cash generation relative to earnings. Liquidity risk is low, but remains dependent on maintaining semiconductor demand and licensing revenues. |

Regulatory Risk: Regulatory risk is significant due to Qualcomm’s licensing model, which has historically been subject to antitrust scrutiny and legal challenges. The 10-K notes ongoing and potential investigations into licensing practices, which could force changes to royalty structures or reduce profitability. Additionally, evolving global regulations around technology, trade, and data security may impact operations and market access. |

MANAGEMENT

Cristiano R. Amon

President, Chief Executive Officer & Director

Cristiano has served as Chief Executive Officer of Qualcomm since 2021 and has been with the company for decades in senior leadership roles across technology and strategy. Prior to becoming CEO, he served as President of Qualcomm CDMA Technologies and played a central role in scaling the company’s semiconductor business and advancing its leadership in 5G technology. He has also held executive roles focused on product development and ecosystem expansion and previously worked as Chief Technology Officer at Vesper SA. Amon is also an Independent Director at Adobe and has been actively involved in global industry organizations, reflecting his influence across both semiconductor innovation and broader technology ecosystems.

__________________________________________________________________________________

Akash Palkhiwala

Chief Financial Officer

Akash has served as CFO of Qualcomm since 2019 and brings extensive financial and operational experience within the company, having previously held roles in investor relations, corporate finance, and operational finance. His background includes leadership across Qualcomm’s global finance operations and strategic planning functions, and he has been instrumental in capital allocation, cost structure optimization, and guiding the company through cyclical semiconductor environments.

__________________________________________________________________________________

Baaaziz Achour

Chief Technology Officer & Executive Vice President

Baaaziz serves as CTO and Executive VP, leading Qualcomm’s technological innovation and long-term R&D strategy. His role focuses on advancing core technologies including wireless connectivity, AI, and system architecture, which underpin Qualcomm’s competitive positioning. He holds advanced academic credentials and has been deeply involved in the company’s engineering leadership and innovation pipeline.

__________________________________________________________________________________

Ann Cathcart Chaplin

Secretary, Executive Vice President & General Counsel

Ann oversees Qualcomm’s global legal, compliance, and governance functions. She joined Qualcomm in 2021 after serving in senior legal roles at major corporations including General Motors and brings extensive expertise in regulatory, corporate governance, and international legal frameworks, which is critical given Qualcomm’s exposure to global regulatory scrutiny.

__________________________________________________________________________________

Don McGuire

Chief Marketing Officer & Senior Vice President

Don leads Qualcomm’s global marketing strategy, brand positioning, and ecosystem partnerships. He has been with the company since 2016 and has held multiple senior marketing roles, including leadership positions in major telecommunications and technology firms. His role focuses on expanding Snapdragon brand equity and strengthening Qualcomm’s positioning across consumer and enterprise markets.

__________________________________________________________________________________

Find Qualcomm's 10 Year Financial Statements below.