NVIDIA STOCK OVERVIEW

- Jan 4

- 8 min read

Updated: Mar 8

SNAPSHOT

Ticker | NVDA | Market Cap | $4.6T |

Sector | Technology | P/E | 53.4 |

52 Week High-Low | $86.62-$212.19 | 3 Year Beta | 1.74 |

CEO | Jensen Huang | Target Price | $252.82 |

BUSINESS MODEL

Products NVIDIA designs high performance computing platforms centered on graphics processing units and related software. Its core products include data center GPUs used for artificial intelligence training and inference, gaming GPUs sold under the GeForce brand, professional visualization hardware for designers and engineers, and automotive computing platforms for advanced driver assistance and autonomous systems. These hardware products are tightly integrated with NVIDIA’s proprietary software ecosystem, including CUDA, AI frameworks, and industry specific libraries, which increases performance, developer adoption, and customer lock in. |

Customer Base NVIDIA serves a diverse global customer base that includes hyperscale cloud providers, enterprise data centers, research institutions, governments, game developers, and individual consumers. Large technology companies and cloud service providers represent a significant portion of data center revenue, while gamers and PC manufacturers drive the gaming segment. Automotive manufacturers and mobility technology firms form a smaller but strategic customer group focused on long term platform adoption rather than short term volume. |

Pricing Method NVIDIA follows a value-based pricing approach rather than cost plus pricing. Products are priced according to performance, energy efficiency, and the economic value they deliver to customers, particularly in AI and data center workloads where computing time directly translates into revenue. High end data center GPUs command premium prices due to limited supply, high demand, and their role in mission critical infrastructure. Consumer products such as gaming GPUs are tiered across price points to address different performance needs while preserving margins at the high end. |

Supply Chain NVIDIA operates a fabless semiconductor model, meaning it designs chips internally but relies on third party manufacturers for production. Advanced chips are primarily fabricated by leading foundries such as TSMC, while packaging, testing, and assembly are handled by specialized partners. The company also depends on a global network of suppliers for memory, substrates, and other components. This model allows NVIDIA to focus capital on design and software, but it also exposes the firm to capacity constraints and geopolitical risks within the semiconductor supply chain. |

Sales Channels NVIDIA sells its products through a mix of direct and indirect channels. Large data center and enterprise customers often purchase directly through negotiated contracts, while cloud providers integrate NVIDIA hardware into their own service offerings. Gaming and professional visualization products are distributed through original equipment manufacturers, add in board partners, system builders, and retail channels. Software and platform offerings increasingly complement hardware sales by reinforcing long term customer relationships and recurring demand for future hardware upgrades. |

REVENUE DRIVERS

INDUSTRY ANALYSIS: PORTER'S 5 FORCES

Threat of New Entrants The threat of new entrants in NVIDIA’s industry is low to moderate. The development of competitive GPUs requires billions of dollars in research and development, specialized engineering talent, and manufacturing access to advanced foundries such as TSMC. These barriers make it difficult for new companies to enter. However, large cloud providers such as Amazon, Microsoft, and Google are investing heavily in their own AI accelerators, which increases pressure even though they are not traditional entrants. |

Bargaining Power of Suppliers Supplier power is moderate to high. NVIDIA relies heavily on TSMC and Samsung for wafer fabrication and on SK Hynix, Micron, and Samsung for high-bandwidth memory. Advanced packaging and substrates are also constrained, which strengthens supplier leverage. Although NVIDIA’s scale provides some negotiating strength, its dependence on a limited set of suppliers increases its exposure to cost pressures and supply chain risks. |

Bargaining Power of Customers Customer power is moderate. NVIDIA’s largest customers are hyperscalers such as Amazon, Microsoft, Google, and Meta, which means that revenue concentration is high. These large customers are capable of negotiating aggressively. However, switching costs remain high because most AI workloads are built on NVIDIA’s CUDA ecosystem, making it costly for customers to move away from NVIDIA hardware. Although hyperscalers are designing their own chips, reliance on NVIDIA’s ecosystem still reduces their bargaining position. |

Threat of Substitutes The threat of substitutes is low to moderate. CPUs alone are not capable of efficiently managing modern AI workloads and are therefore not a practical replacement. Other accelerators, such as Google’s TPU, AWS Trainium, and AMD’s MI300 GPUs, present alternative options but are either tied to specific cloud ecosystems or are still building market share. In the longer term, technologies such as quantum computing may emerge as potential substitutes, but at present they remain commercially insignificant. |

Competitive Rivalry Competitive rivalry in NVIDIA’s industry is high. Direct competitors include AMD, which is gaining momentum with its MI300 series, and Intel, which is advancing its Gaudi line of accelerators. Indirect competition also comes from hyperscalers that are reducing external purchases by producing their own custom chips. Although NVIDIA currently commands 70 to 80 percent of the AI GPU market, competitors are investing heavily to gain share. NVIDIA still enjoys strong pricing power, but competitive pressure may impact margins in the future. |

VALUATION: DISCOUNTED CASH FLOW

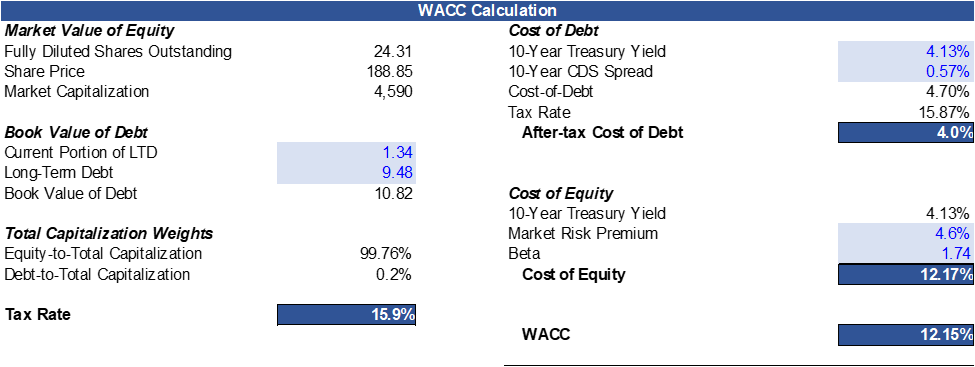

WACC

INVESTMENT RISKS

Systematic Risk |

Market Risk: The stock market is currently trading at an all-time high, and growth is expected to continue at least in the near term. However, despite this growth, the Wall Street Journal has reported that 39% of the market’s value is concentrated in the 10 highest-valued public firms. Nvidia, as the highest-valued company in the world, is part of this concentration. The firm is trading at over 50 times its earnings, with sales having more than tripled in the last three years and its stock valuation doubling in just the past three months.

As the leading force in the rapid advancement of artificial intelligence, Nvidia is expected to continue growing in both value and earnings as the AI race accelerates market momentum. However, investors should exercise caution regarding any potential downturn in this inflated market valuation. With a three-year beta of 1.74, Nvidia is highly exposed to systematic risk and is likely to face a significant decline if the overall stock market experiences a downturn. |

Geopolitical Risk: Nvidia faces significant geopolitical risk. As highlighted in its business model, the company has substantial international exposure in both sales and manufacturing. Its dependence on Taiwan-based manufacturing would be severely detrimental if tensions between China and Taiwan were to escalate into conflict. Moreover, strained relations between the U.S. and China present another major risk to operations. The company’s CEO is frequently forced to navigate the demands of two powerful governments with differing regulations and concessions.

China has increased pressure on domestic firms to replace Nvidia products with domestic alternatives, while also accusing Nvidia of antitrust violations; both examples of the challenging environment the company faces in this critical market. Additionally, due to its heavy reliance on international trade, global tariff uncertainty represents another major risk factor for the firm’s operations. |

Unsystematic Risk |

Business Risk: Nvidia’s management team is composed of highly skilled leaders with tenures ranging from 4 to 19 years, averaging 8 years. The team’s track record of increasing operating margins and return on capital demonstrates their ability to grow the company efficiently and solidify its leadership position in the technology sector. In the past year, Nvidia has successfully transformed heavy R&D investments and capital expenditures into substantial shareholder value.

This strong management performance is reflected in the company’s robust cash position, minimal reliance on debt, expanding economies of scale, powerful brand presence, and strong prospects for future returns. Notably, Nvidia’s recent pledge to invest in competitor Intel and startup OpenAI demonstrates the company’s strategy of diversifying its investments to generate more circular and sustainable earnings. |

Financial Risk: Nvidia’s financial position is envied by most competitors. As the highest-valued company in the world, it generates extraordinary levels of cash, enabling it to fund operations without heavy reliance on debt. The company has significantly reduced its debt-to-equity ratio from 60.49% in 2021 to 10.58% in 2025. Similarly, its total debt-to-capital ratio declined from 37.69% in 2021 to 9.57% in 2025.

This dramatic improvement in financial strength coincides with rapid revenue expansion beginning around 2021, when growth accelerated from 20% annually to 165% in 2025. |

Liquidity Risk: Closely tied to its financial position, Nvidia’s liquidity risk is also very low. Conservative cash ratio calculations consistently show highly positive results, confirming the company’s ability to cover its extensive operations with cash on hand. |

Industry Risk: Nvidia operates in a highly volatile yet rapidly expanding industry, where it faces fierce competition. Although the firm currently holds a dominant market share, both foreign and domestic competitors are investing substantial capital and talent into AI research. The recent mega deal between AMD, Nvidia’s direct competitor, and Open AI, is a testimony of the competitive threats to the firm’s dominance. This competitive pressure explains why Nvidia has doubled its R&D spending since 2023 and is expected to continue increasing its research investments.

The emergence of firms like DeepSeek demonstrates how disruptive innovations from rivals could challenge Nvidia’s core revenue stream. Because over 80% of its revenue comes from the data center AI segment, any decline in demand for these products would have a severe impact on Nvidia’s earnings prospects. |

Regulatory Risk: Regulatory risk remains a material concern for Nvidia in three primary areas: (1) export restrictions that reduce access to key growth markets such as China, (2) antitrust scrutiny that could limit pricing power or block strategic acquisitions, and (3) emerging AI and ESG regulations that may increase compliance costs. Given Nvidia’s central role in the global AI ecosystem, the company is highly exposed to political, legal, and regulatory developments across multiple jurisdictions. |

MANAGEMENT

Jensen Huang

President, Chief Executive Officer, and Director

Jensen Huang co-founded NVIDIA in 1993 and has served as its President, CEO, and Director since inception. He led the company’s evolution from a graphics chip startup to a global leader in GPUs, AI computing, and data center technology. Prior to NVIDIA, he held engineering roles at LSI Logic and AMD. Mr. Huang earned an M.S. in Electrical Engineering from Stanford University and a B.S. in Electrical Engineering from Oregon State University. As of October 2025, he owns about 3.5% of NVIDIA shares, with total annual compensation of $49.9 million.

__________________________________________________________________________________

Debora Shoquist

Executive Vice President, Operations

Debora Shoquist has served as NVIDIA’s Executive Vice President of Operations since 2007, overseeing global manufacturing and supply chain functions. Before joining NVIDIA, she held senior leadership roles at Coherent, HP, Quantum, and JDS Uniphase. She holds a B.S. in Electrical Engineering from Kansas State University and an MBA from Santa Clara University. As of September 2025, she owns roughly 2.25 million NVIDIA shares, with total compensation of $19.2 million.

__________________________________________________________________________________

Colette M. Kress, MBA

Chief Financial Officer and Executive Vice President

Colette oversees the company’s global financial strategy, investor relations, and operations. Before joining NVIDIA, she held senior finance leadership roles at Cisco Systems, including SVP and CFO of Business Technology and Operations Finance, and earlier at Microsoft as CFO of the Server & Tools division. Ms. Kress earned her MBA from Southern Methodist University and a bachelor’s degree from the University of Arizona. As of September 2025, she holds 5.27 million NVIDIA shares, with total annual compensation of $21.4 million.

__________________________________________________________________________________

Timothy S. Teter

Secretary, Executive Vice President, and General Counsel

Timothy Teter has served as NVIDIA’s Executive Vice President, General Counsel, and Secretary since 2018, overseeing all legal, regulatory, and compliance matters. Before joining NVIDIA, he was a partner at Cooley LLP for over 20 years, specializing in corporate and securities law. Mr. Teter holds a bachelor’s degree from the University of California, Davis, and a J.D. from Stanford Law School. As of September 2025, he owns about 3.05 million NVIDIA shares, with total annual compensation of $19.2 million.

__________________________________________________________________________________

Donald F. Robertson, Jr., CPA

Chief Accounting Officer and Vice President

Donald also serves in leadership roles across NVIDIA’s international subsidiaries, including NVIDIA ARC GmbH, NVIDIA Ltd., and NVIDIA Développement France SASU. Before joining NVIDIA, he held senior finance positions at Adaptec, Fusion-io, Mellanox Technologies, Western Digital, and SanDisk, and began his career with PricewaterhouseCoopers LLP. Mr. Robertson holds a graduate degree from San Jose State University and a bachelor’s degree from the University of California, San Diego. As of September 2025, he holds approximately 457,000 NVIDIA shares.

__________________________________________________________________________________

Find Nvidia's 10 Year Financial Statements below.