McDONALD's STOCK OVERVIEW

- Apr 12

- 6 min read

SNAPSHOT

last updated on 6/28/2026

Ticker | MCD | Sector | Hospitality Services |

52 Week High-Low | $264.53 - $341.75 | Industry | Fast Food Restaurants |

CEO | Christopher J. Kempczinski | Target Price | $287.20 |

BUSINESS MODEL

Products McDonald’s Corporation is a global quick-service restaurant company that primarily operates as a franchisor, owning, operating, and franchising restaurants that serve a standardized yet locally adaptable menu of food and beverages including burgers, chicken products, fries, breakfast items, beverages, and desserts. The company’s core business model is built on its heavily franchised structure, where approximately 95% of its 45,000+ restaurants are operated by independent franchisees, developmental licensees, or affiliates, while the company maintains a smaller base of company-owned restaurants to test operations, innovations, and maintain system control. Revenues are generated through a combination of sales from company-operated restaurants and fees from franchisees, including rent, royalties based on a percentage of sales, and initial franchise fees, making McDonald’s both a restaurant operator and a real estate-driven cash flow business with stable, recurring income streams. |

Customer Base McDonald’s serves a global mass-market customer base across more than 100 countries, targeting consumers seeking convenience, affordability, and consistency in food service. Its customers include individuals and families purchasing meals through dine-in, drive-thru, delivery, and digital channels, with demand driven by frequency, value perception, and brand loyalty. The system also includes franchisees, suppliers, and employees forming the “three-legged stool,” which is central to operational execution and scalability. The broad geographic diversification and high transaction volume create a resilient and diversified demand base. |

Pricing Method McDonald’s pricing is largely determined at the franchisee level within a framework of brand strategy and value positioning, with the company influencing pricing through promotional strategies, product mix, and value offerings. Revenue from franchised restaurants is tied to a percentage of franchisee sales through rent and royalty structures, aligning McDonald’s financial performance directly with systemwide sales growth rather than solely company-operated margins. This structure allows the company to maintain high operating margins and predictable revenue streams while sharing operational risks with franchisees. |

Supply Chain McDonald’s operates a global supply chain supported by a network of independent suppliers providing food, packaging, and equipment, with strict quality and safety standards enforced through audits, supplier codes of conduct, and centralized oversight. The company collaborates with suppliers to ensure consistency, efficiency, and innovation while maintaining global scale advantages in procurement. Supply chain risk management is centralized and supported by ongoing monitoring, third-party verification, and sustainability initiatives, making the system highly coordinated but dependent on global sourcing conditions. |

Sales Channels McDonald’s generates sales through multiple channels including in-store dining, drive-thru, delivery, and digital platforms such as mobile apps and loyalty programs. The company’s strategy emphasizes omnichannel access through its “4D” model—Digital, Delivery, Drive-Thru, and Development—allowing customers to engage through convenient and personalized ordering experiences. Franchisees operate the majority of locations, but all channels contribute to systemwide sales, which drive royalty-based revenues for the company. |

INDUSTRY ANALYSIS: PORTER'S 5 FORCES

Threat of New Entrants — Low The threat of new entrants is low due to McDonald’s global brand strength, scale, real estate ownership model, and franchise network, which create significant barriers to entry in terms of capital requirements, supply chain infrastructure, and brand recognition. Replicating its global footprint and operational consistency would require substantial investment and time. |

Bargaining Power of Buyers — Moderate Buyer power is moderate as customers have many alternative food options and low switching costs, but McDonald’s brand recognition, convenience, and value offerings help retain demand. Franchisees also have some influence within the system but operate under strict brand and operational standards, limiting their bargaining power. |

Bargaining Power of Suppliers — Moderate Supplier power is moderate due to the company’s global scale and diversified sourcing network, which reduces dependence on individual suppliers. However, commodity price volatility, food safety requirements, and reliance on consistent supply chains can increase supplier influence in certain conditions. |

Threat of Substitutes — High The threat of substitutes is high because consumers can easily switch to other quick-service restaurants, fast casual dining, grocery options, or delivery-based alternatives. Changing consumer preferences toward healthier options and alternative dining formats further increase substitution risk. |

Competitive Rivalry — Very High Competitive rivalry is very high as McDonald’s competes with global and local quick-service and fast-casual restaurants, as well as convenience and delivery platforms. Competition is driven by pricing, convenience, product innovation, and customer experience, requiring continuous marketing and operational investment to maintain market share. |

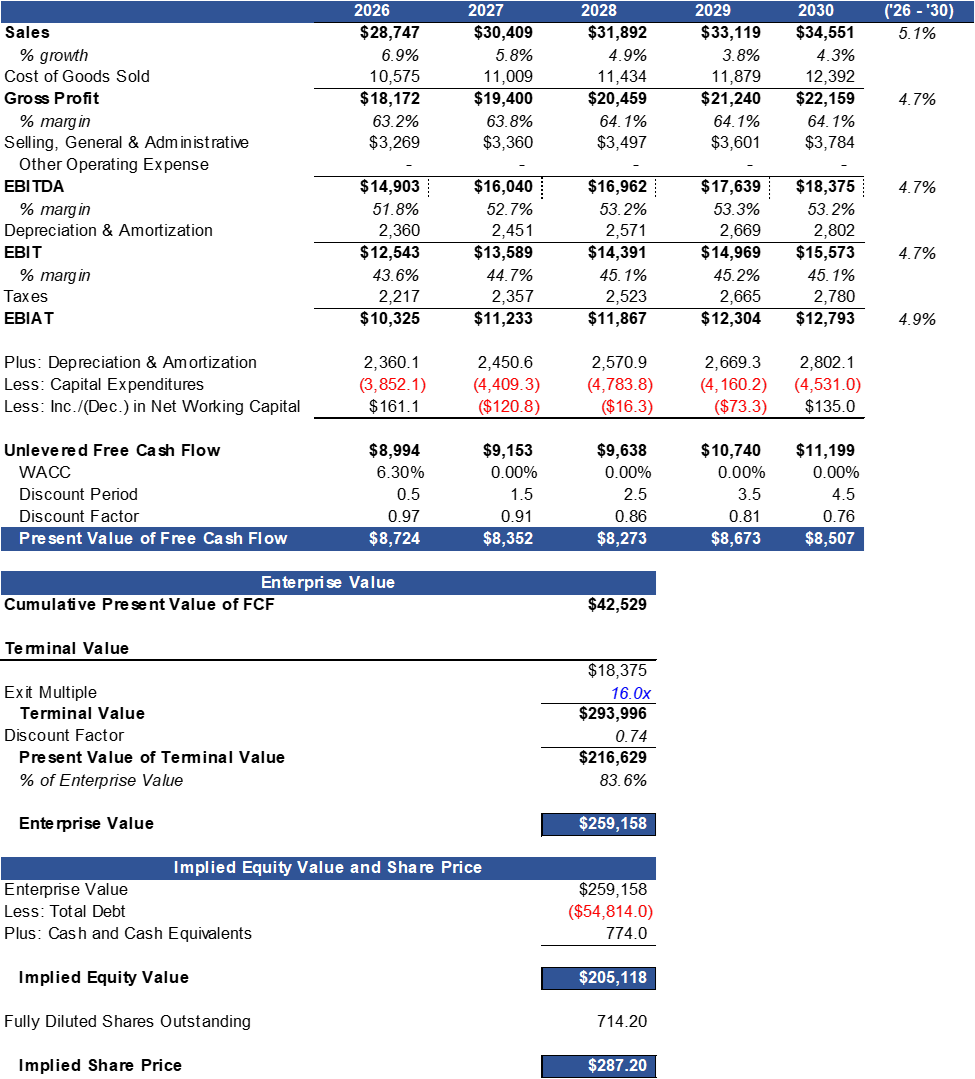

VALUATION: DISCOUNTED CASH FLOW

INVESTMENT RISKS

Systematic Risk |

Market Risk: McDonald's market risk is tied to its premium valuation and dependence on consistent systemwide sales growth. The company trades at elevated multiples across earnings, EV/EBITDA, and price to sales, reflecting a high-quality, defensive business priced for stability. Profitability is exceptionally strong, with high operating margin, pretax margin, and net margin in 2025, supported by its franchise-heavy model. However, high valuation multiples combined with slowing consumer spending or traffic declines could lead to multiple compression, making the stock sensitive to macro-driven demand changes. |

Geopolitical Risk: McDonald’s faces geopolitical risk due to its operations in over 100 countries, exposing it to currency fluctuations, trade policies, regulatory changes, and regional economic conditions. The 10-K highlights that foreign currency translation impacts reported earnings and that global macroeconomic conditions can affect consumer spending and restaurant performance across markets. While diversification mitigates concentration risk, localized disruptions can still impact systemwide sales and franchisee performance. |

Unsystematic Risk |

Business Risk: McDonald's business risk centers on maintaining traffic growth, franchisee economics, and adapting to changing consumer preferences. While free cash flow margin remains strong, asset turnover is relatively low, reflecting a capital-intensive real estate model. Return on invested capital shows solid but not exceptional efficiency given the company's scale. Additionally, reliance on franchisee execution introduces variability in customer experience, and shifts toward healthier eating or competitive formats could pressure long-term demand. |

Financial Risk: McDonald's financial risk is moderate due to its leveraged capital structure. Net debt to EBITDA and total debt to EBITDA both indicate meaningful leverage. Interest coverage remains adequate, with EBIT covering interest expense comfortably, but this is lower than historical peaks, suggesting reduced financial flexibility. The company's negative equity position, reflected in negative book value and extreme debt-to-equity ratios, highlights reliance on debt financing and shareholder returns, which increases sensitivity to rising interest rates. |

Liquidity Risk: Liquidity risk is moderate, with a current ratio and quick ratio both near one, indicating tight short-term coverage. The cash ratio is relatively low, suggesting limited immediate liquidity buffers. However, strong operating cash flow provides support, with CFO to current liabilities at a high level, indicating that ongoing operations generate sufficient cash to meet obligations. Liquidity is therefore dependent on continued stable cash flow generation rather than balance sheet strength. |

Regulatory Risk: McDonald’s faces significant regulatory risk due to global operations across multiple jurisdictions, including regulations related to food safety, labor practices, franchising, environmental standards, and taxation. The company must comply with diverse legal frameworks, and increasing regulatory scrutiny in areas such as health, sustainability, and employment could increase costs or restrict operations. Additionally, franchise regulations and zoning laws can impact expansion and operational flexibility. |

MANAGEMENT

Christopher J. Kempczinski

Chairman, President & Chief Executive Officer

Christopher has served as Chairman, President, and Chief Executive Officer since 2019 and has been with McDonald’s since 2015. He previously held senior leadership roles including President of McDonald’s USA and has experience from Kraft Heinz and PepsiCo. He leads the company’s global strategy, operations, and franchise system.

__________________________________________________________________________________

Ian Borden

Global Chief Financial Officer & Executive Vice President

Ian has served as Global Chief Financial Officer since 2022 and has been with McDonald’s since 2007. He previously held leadership roles across international markets including Asia Pacific, Middle East, and Africa, and oversees financial strategy, capital allocation, and investor relations.

__________________________________________________________________________________

Brian S. Rice

Global Chief Information Officer & Executive Vice President

Brian has served as Global Chief Information Officer since 2022 and is responsible for technology infrastructure, digital transformation, and IT strategy. He previously held leadership roles at Cardinal Health and Mars, bringing extensive experience in enterprise technology systems.

__________________________________________________________________________________

Jonathan Banner

Global Chief Impact Officer & Executive Vice President

Jonathan has served as Global Chief Impact Officer since 2022, overseeing corporate responsibility, sustainability, and communications. He previously held leadership roles at PepsiCo and ABC News, focusing on global communications and impact initiatives.

__________________________________________________________________________________

Gillian McDonald

Global Chief Restaurant Experience Officer & EVP

Gillian has served as Global Chief Restaurant Experience Officer since 2025 and focuses on improving customer experience, restaurant operations, and brand execution globally. She previously held leadership roles in hospitality and operations.

__________________________________________________________________________________

Desiree Ralls-Morrison Jr.

Global Chief Legal Officer & Executive VP

Desiree has served as Global Chief Legal Officer since 2021 and oversees legal, compliance, and governance functions. She previously held senior legal roles at major corporations including Johnson & Johnson and brings extensive regulatory and corporate law expertise.

__________________________________________________________________________________

Find McDonald's 10 Year Financial Statements below.